Antwort Are leases treated as debt? Weitere Antworten – Are leases considered debt

The liability associated with a Finance Lease is considered debt, which is consistent with previous Capital Lease treatment.Operating leases are shown as an asset on the balance sheet, valued as the present value of the lease payments (not the market value of the asset). The lease liability is shown on the balance sheet (similarly, the present value of the lease payments).GAAP rules govern accounting for operating leases. All leases 12 months and longer must be recognized on the balance sheet.

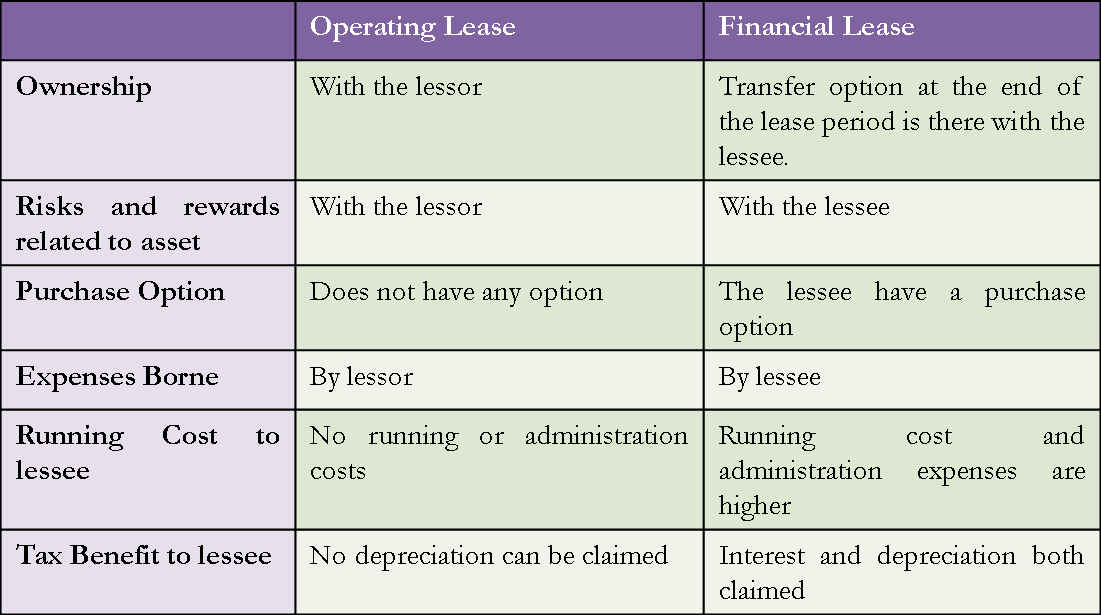

Is an operating lease an asset : An operating lease is recorded on the balance sheet as an asset and the monthly rental payments are treated as operational expenses, not debt.

Why is lease a debt

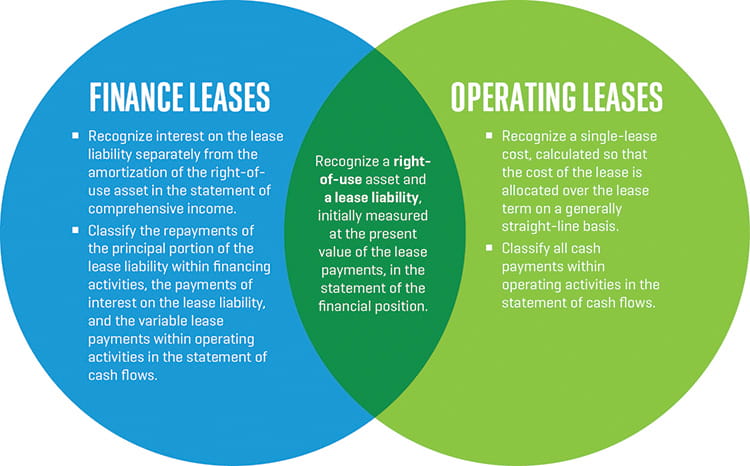

The lease liability is the present value of the future lease payments and is recorded alongside the right-of-use asset for operating and finance leases. Under ASC 842, the lease liability is not considered debt. Under IFRS 16 and GASB 87, however, a lease liability is considered long-term debt.

Why is lease liability considered debt : The lessee typically makes regular lease payments over a specific period, which includes interest charges. Since the lessee bears the risks and rewards, the lease liability is considered a form of debt on their balance sheet.

A lease will be recorded on the balance sheet as a right-of-use (ROU) asset and lease liability. The lease liability is the payment obligation over the term of the lease contract, while the ROU asset represents the control of the asset under the lease contract.

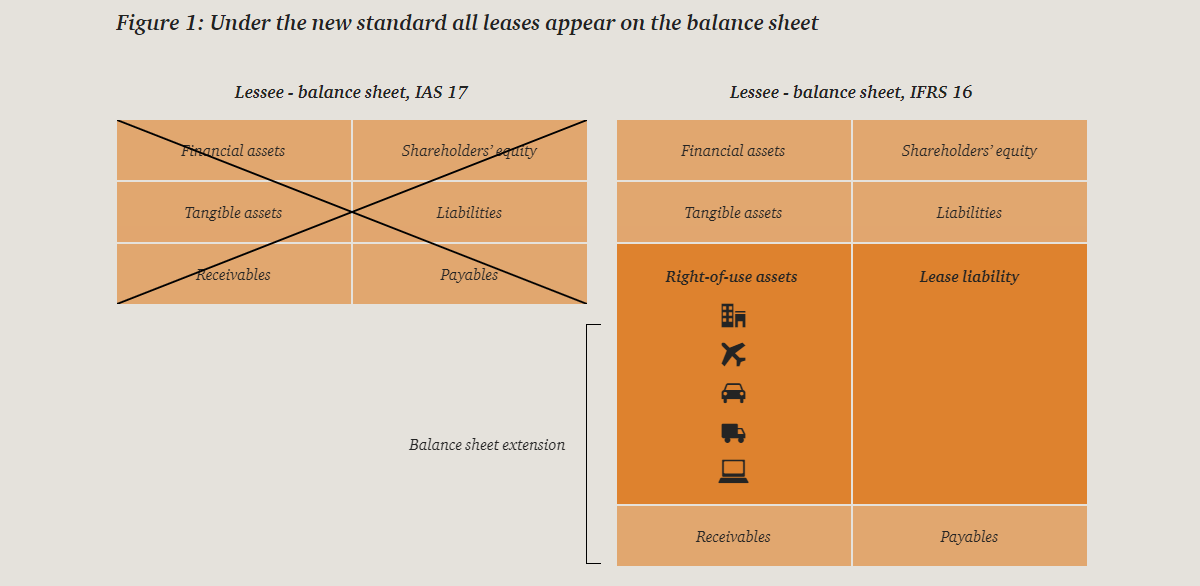

With IFRS 16, lease liabilities for all (operational) leases are now recognized, which increases the numerator of the ratio. The total debt of the company will also increase because the recognized lease liabilities are included in the company's debt calculations.

How are leases recognized in accounting

Leased Asset on the Balance Sheet: The value of the leased asset is recorded as a fixed asset on the balance sheet. The amount recorded is generally the present value of the minimum lease payments or the fair market value of the leased asset, whichever is lower.The asset and related lease liability are recognized at the present value of the future lease payments and the debt (the lease) is a long-term liability with a short-term component.When a lease is classified as a capital lease, the present value of the lease expenses is treated as debt, and interest is imputed on this amount and shown as part of the income statement.

A right-to-use lease asset is an intangible capital asset. The asset represents the right to use an underlying asset identified in a lease contract, as specified for a period of time.

What is the difference between debt and lease : Unlike lease financing, where the lessee does not own the equipment, debt financing allows a business to acquire asset ownership immediately to acquire asset ownership immediately. This ownership factor can be a significant advantage for companies planning long-term use of the equipment, as it builds equity over time.

Do capital leases count as debt : From a lease accounting perspective, a capital lease is treated as if the lessee has purchased the asset using debt financing. The asset and the associated lease liability are recorded on the lessee's balance sheet. Each lease payment is allocated between the reduction of the lease liability and interest expense.

Are leases debt in IFRS

Here's how IFRS 16 can affect this ratio: The enterprise value (EV) may increase because lease liabilities are now recognized on the balance sheet and are now recognized on the balance sheet as interest-bearing debt. Since EV includes the market value of debt, the addition of lease liabilities will increase the EV.

Unlike lease financing, where the lessee does not own the equipment, debt financing allows a business to acquire asset ownership immediately to acquire asset ownership immediately. This ownership factor can be a significant advantage for companies planning long-term use of the equipment, as it builds equity over time.Accounting for a finance lease has four steps:

- Record the present value of all lease payments as the cost of the lease.

- Record only the interest portion of each payment as an expense.

- Depreciate the recognised cost of the asset over its applicable life.

- Recognise the asset's disposal upon its retirement.

How do I account for leases under IFRS : Overview. IFRS 16 specifies how an IFRS reporter will recognise, measure, present and disclose leases. The standard provides a single lessee accounting model, requiring lessees to recognise assets and liabilities for all leases unless the lease term is 12 months or less or the underlying asset has a low value.