Antwort Does IFRS 16 apply to all leases? Weitere Antworten – What leases fall under IFRS 16

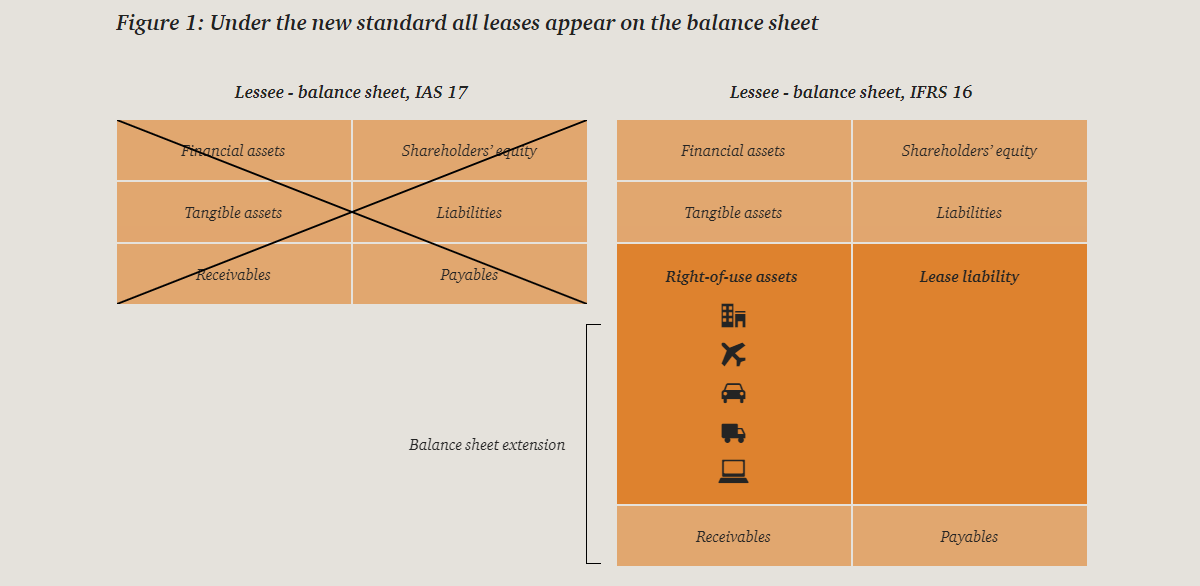

IFRS 16 introduces a single lessee accounting model and requires a lessee to recognise assets and liabilities for all leases with a term of more than 12 months, unless the underlying asset is of low value.IFRS 16 offers two optional exemptions from recognition of right-of-use assets and lease liabilities. The first is an exemption from short-term leases, and the second is the exemption from leases of low value assets. Key learning objectives: Identify the two IFRS 16 exemptions, and explain why they are exempt.On 13 January 2016, the International Accounting Standards Board (IASB) issued IFRS 16 Leases, which essentially does away with operating leases and, subject to limited exceptions, requires all leases to be capitalised on the balance sheet.

Is IFRS 16 mandatory : Is IFRS 16 mandatory IFRS 16 is mandatory for all companies within its scope, so mainly international companies or public limited companies.

How do you know if lease is under IFRS 16

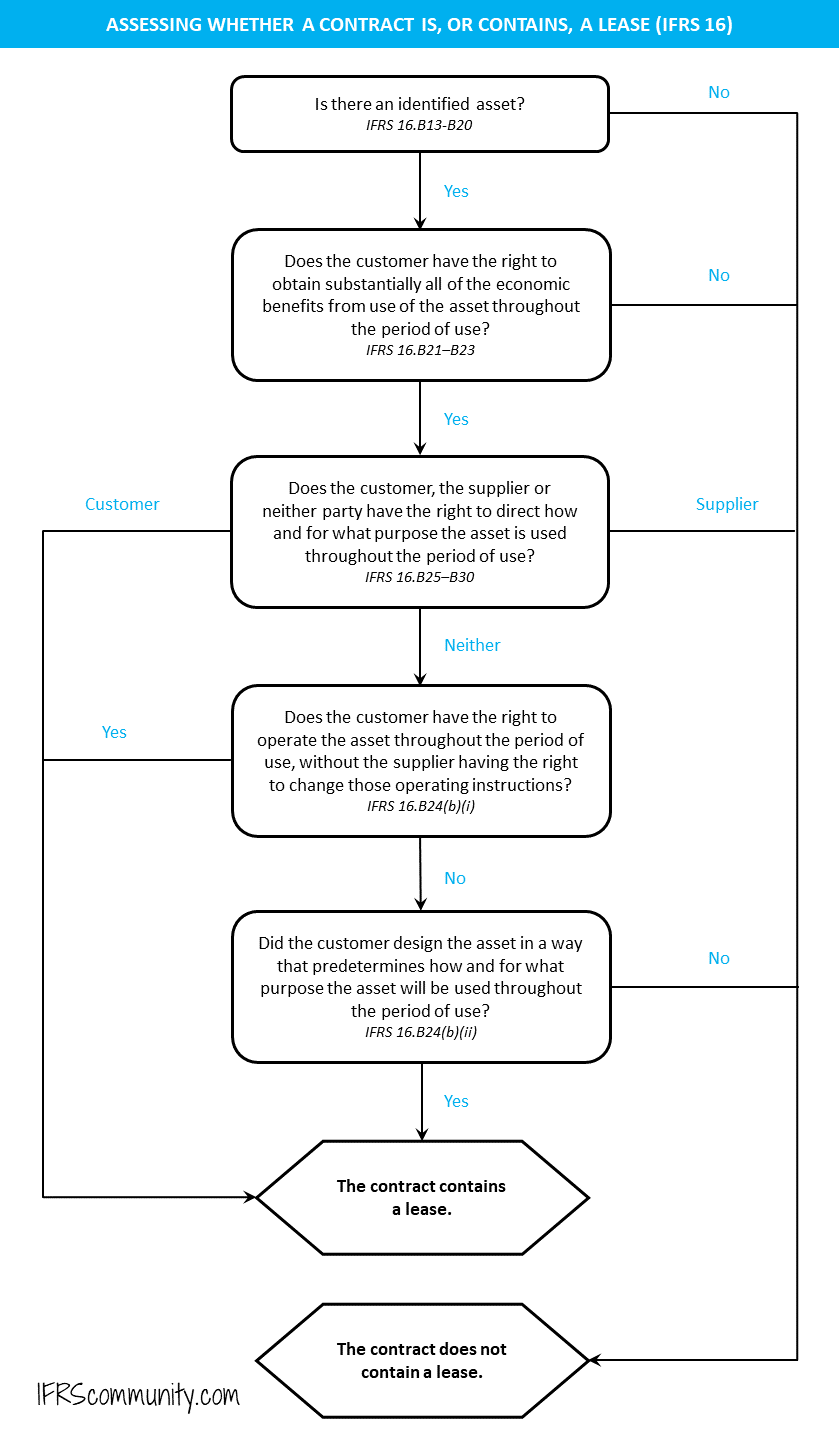

Paragraph 9 of IFRS 16 states that 'a contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration'.

Who does IFRS 16 apply to : Who does IFRS 16 apply to Initially, at least, these changes will only apply to organisations that already report using IFRS, typically international companies or PLCs. The majority of SMEs report to the UK's generally accepted accounting principles (UK GAAP) and this is unlikely to change until around 2022/23.

IFRS 16 states that the objective of the updated disclosure requirements is for lessees to “disclose information in the notes that, together with the information provided in the statement of financial position, statement of profit or loss and statement of cash flows, gives a basis for users of financial statements to …

If the lease commencement date determined under IFRS 16 precedes the payment initiation, the right-of-use asset and related liability should be recognised at the commencement date.

What is the difference between IAS 17 and IFRS 16 finance lease

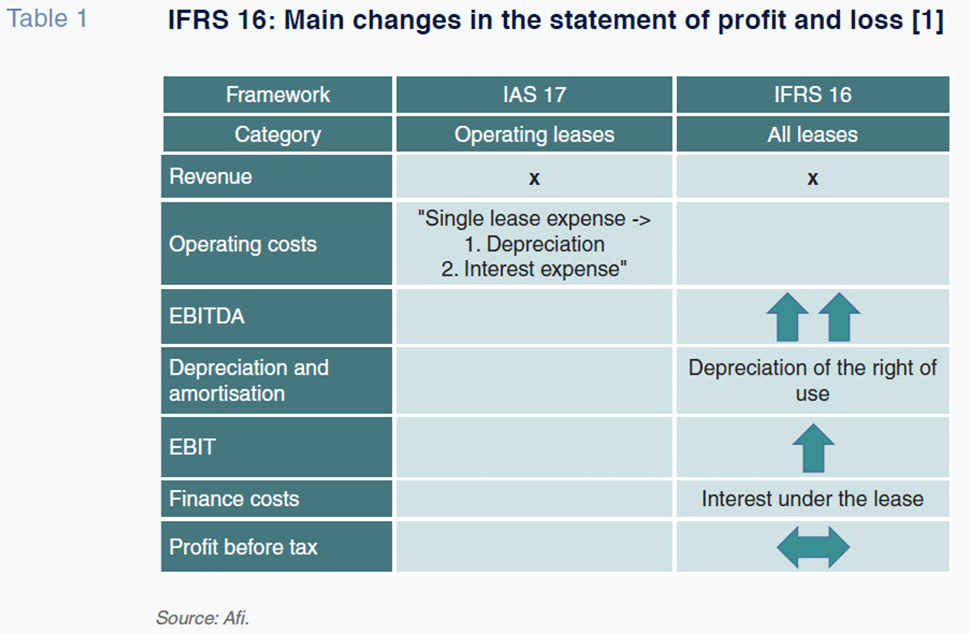

This is because, applying IFRS 16, a company presents the implicit interest in lease payments for former off balance sheet leases as part of finance costs. In contrast, under IAS 17, the entire expense related to off balance sheet leases is included as part of operating expenses.A: No, all companies in India don't need to adopt IFRS/Ind AS. However, listed companies and certain unlisted companies must adopt Ind AS. Banks, insurance companies, and non-banking financial companies are also required to adopt Ind AS as per the timelines specified by the RBI and IRDAI.IAS 17 was reissued in December 2003 and applies to annual periods beginning on or after 1 January 2005. IAS 17 will be superseded by IFRS 16 Leases as of 1 January 2019.

Financial statements in accordance with IFRS must be prepared by:

- Public interest entities – banks, insurance companies (except health), asset management companies, stock exchange and their branches.

- An entity that is a trading company and has at least two consecutive accounting periods.

Who does IFRS apply to : They are particularly relevant for companies with shares or securities publicly listed. IFRS have replaced many different national accounting standards around the world but have not replaced the separate accounting standards in the United States where U.S. GAAP is applied.

What is the difference between IAS 17 and IFRS 16 : IFRS 16 is expected to reduce operating cash outflows, with a corresponding increase in financing cash outflows, compared to the amounts reported applying IAS 17. This is because, under IAS 17, companies present cash outflows on off balance sheet leases as operating activities.

Why was IAS 17 replaced by IFRS 16

Why the new lease standard Short answer: To eliminate off-balance sheet financing. Under IAS 17, lessees needed to classify the lease as either finance or operating.

The Canadian Accounting Standards Board (AcSB) requires publicly accountable enterprises to use IFRS in the preparation of all interim and annual financial statements. Most private companies also have the option to adopt IFRS for financial statement preparation.Companies must follow IFRS rules to accurately show their financial position and performance. Non-compliance with IFRS can be bad for a company's reputation. It can also stop investors from doing business with them. Stakeholders may not understand the financial information, leading to bad decisions.

Is IFRS mandatory : IFRS Standards are required or permitted in 132 jurisdictions across the world, including major countries and territories such as Australia, Brazil, Canada, Chile, the European Union, GCC countries, Hong Kong, India, Israel, Malaysia, Pakistan, Philippines, Russia, Singapore, South Africa, South Korea, Taiwan, and …