Antwort How are leases classified? Weitere Antworten – How is a lease classified under IFRS 16

There are 2 types of leases defined in IFRS 16: A finance lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an underlying asset. An operating lease is a lease other than a finance lease.Overview. IFRS 16 specifies how an IFRS reporter will recognise, measure, present and disclose leases. The standard provides a single lessee accounting model, requiring lessees to recognise assets and liabilities for all leases unless the lease term is 12 months or less or the underlying asset has a low value.Under IAS 17, leases are classified as either Finance Lease or Operating Lease based on the risks and rewards incidental to ownership of the asset. Under IFRS 16, all leases are classified as Finance Leases, and the lessee is required to RECOGNIZE a lease liability and a Right of Use (RoU) asset.

How to account for finance lease by lessor : When the lease agreement is classified as a finance lease, the lessor will calculate the net investment in the lease using the present value of future expected lease receipts and record this amount as a receivable. Lessors are also required to derecognize the carrying value of the underlying asset.

How do you classify a lease

Leases have two classifications under US GAAP . A capital lease, now known as a finance lease, resembles a financed purchase; the lease term spans most of the asset's useful life. An operating lease resembles a rental agreement in that the asset is used for a set time with useful life remaining at lease end.

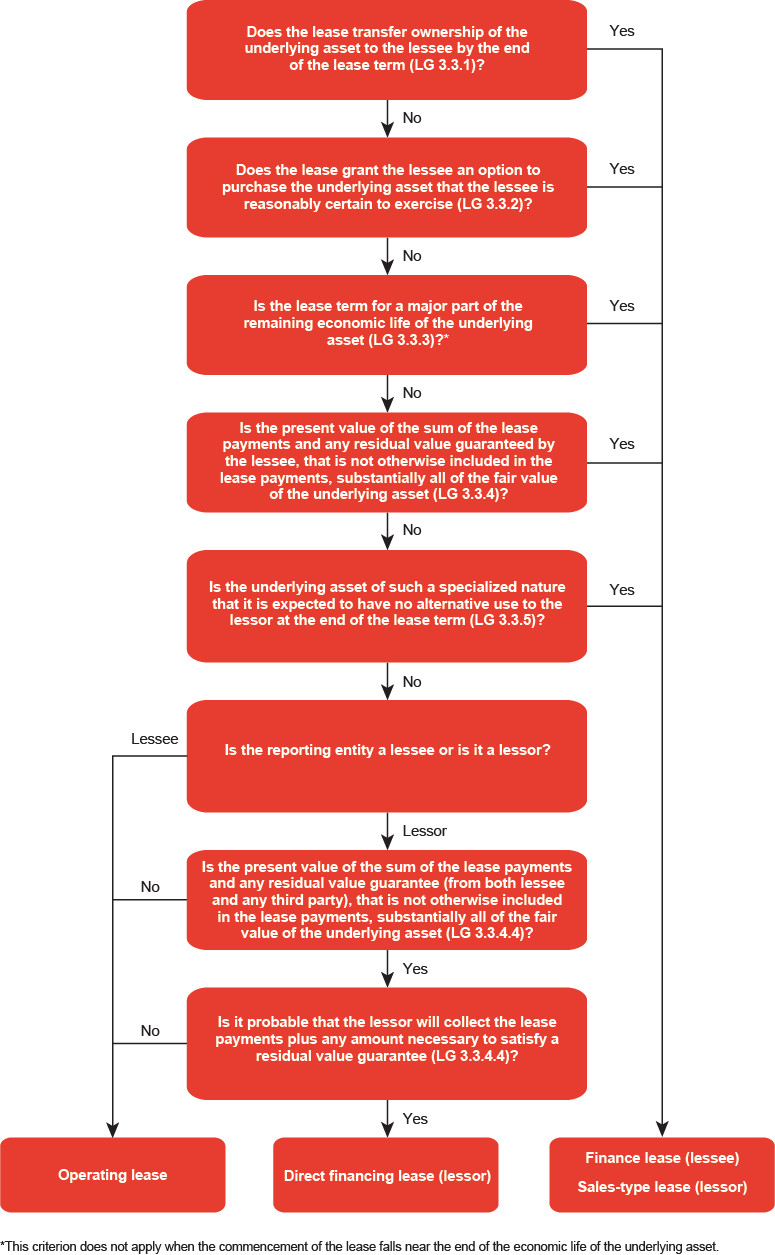

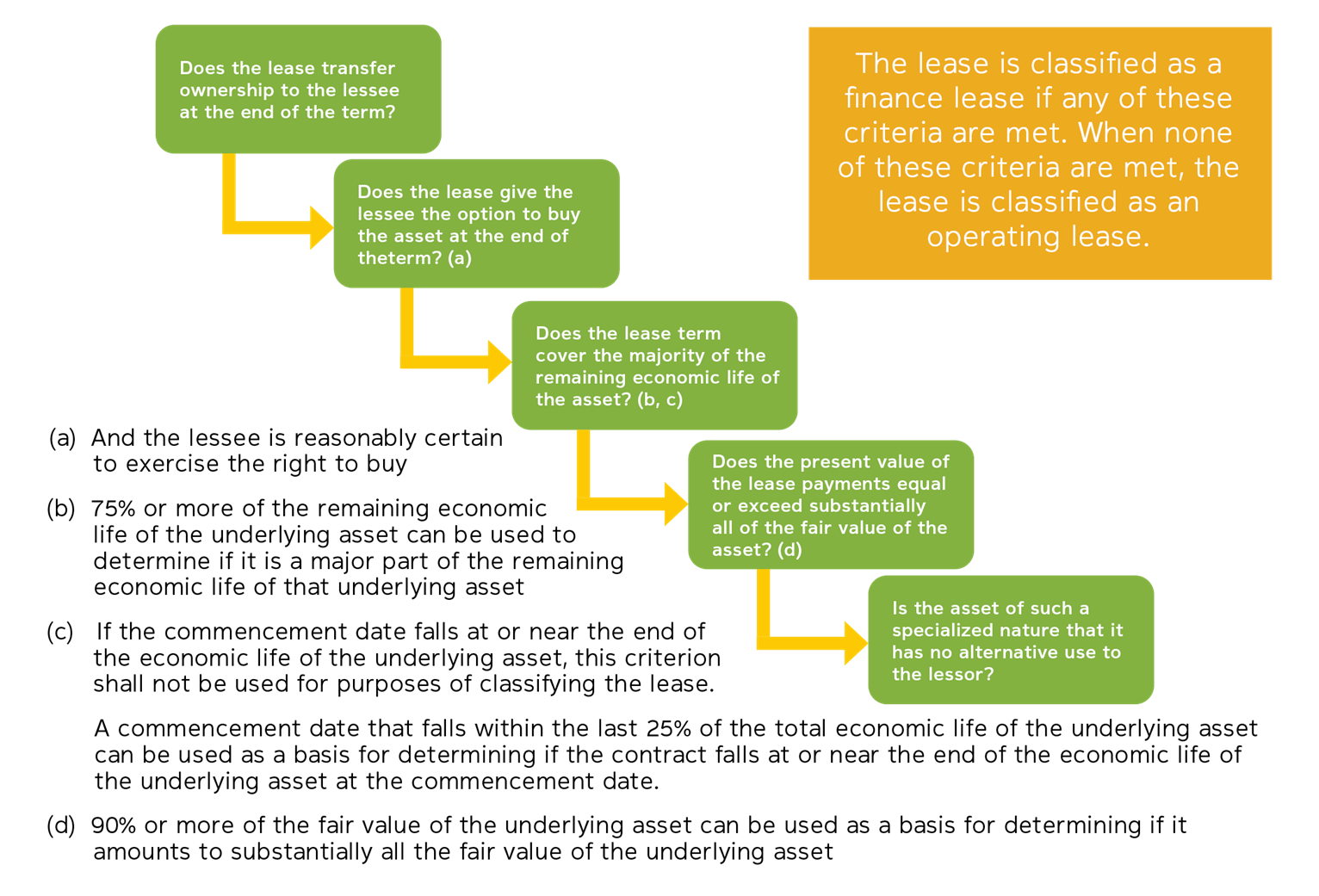

What is a lease classified as : A lease is classified as a finance lease by a lessee and as a sales-type lease by a lessor if ownership of the underlying asset transfers to the lessee by the end of the lease term. This criterion is also met if the lessee is required to pay a nominal fee for the legal transfer of ownership.

Accounting for a finance lease has four steps:

- Record the present value of all lease payments as the cost of the lease.

- Record only the interest portion of each payment as an expense.

- Depreciate the recognised cost of the asset over its applicable life.

- Recognise the asset's disposal upon its retirement.

AS 19 is a standard issued by the Institute of Chartered Accountants of India (ICAI) that provides guidelines for accounting and reporting leases. The objective of AS 19 is to ensure that the financial statements of a company reflect the substance of its lease transactions, and not just the legal form.

When did IFRS 16 replace IAS 17

IFRS 16 Leases will replace IAS 17 leases for reporting periods beginning on, or after, the 1st of January, 2019.Since then, IAS 16 and its accompanying documents have been amended by: IFRS 13 Fair Value Measurement (issued May 2011), Annual Improvements to IFRSs 2009–2011 Cycle (issued May 2012), Annual Improvements to IFRSs 2010–2012 Cycle (issued December 2013), IFRS 15 Revenue from Contracts with Customers (issued May 2014), …In accordance with IFRS 16.61, a lessor should classify each of its leases as either a finance lease or an operating lease. Leases that transfer substantially all of the risks and rewards incidental to ownership of the underlying asset are finance leases, and all other leases are operating leases.

The five criteria relates to a bargain purchase option, transfer of ownership, net present value of lease payments, economic life, and whether the asset is specialized.

How do you classify a financial lease : Under FASB ASC 842, a lessee can classify a lease as either an Operating lease or a Finance lease. A Finance lease is accounted for in a manner similar to a Capital lease under ASC 840 where an ROU asset and a lease liability are recorded equal to the NPV of the lease payments.

What are the classification of lease agreements : Leases have two classifications under US GAAP . A capital lease, now known as a finance lease, resembles a financed purchase; the lease term spans most of the asset's useful life. An operating lease resembles a rental agreement in that the asset is used for a set time with useful life remaining at lease end.

How do I record a lease

Once we have gathered our information (i.e., we know the lease term, the lease payment, and the discount rate), we simply discount the liability over the lease term, using the discount rate. We then record the lease liability, or the resulting amount, on the balance sheet. Then, we record the lease asset.

Leased Asset on the Balance Sheet: The value of the leased asset is recorded as a fixed asset on the balance sheet. The amount recorded is generally the present value of the minimum lease payments or the fair market value of the leased asset, whichever is lower.Leased Asset on the Balance Sheet: The value of the leased asset is recorded as a fixed asset on the balance sheet. The amount recorded is generally the present value of the minimum lease payments or the fair market value of the leased asset, whichever is lower.

What category is a lease in accounting : Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. The two most common types of leases in accounting are operating and finance (or capital) leases.