Antwort How do you classify finance lease and operating lease? Weitere Antworten – What is the difference between operating and finance leases in IFRS 16

Classification of leases

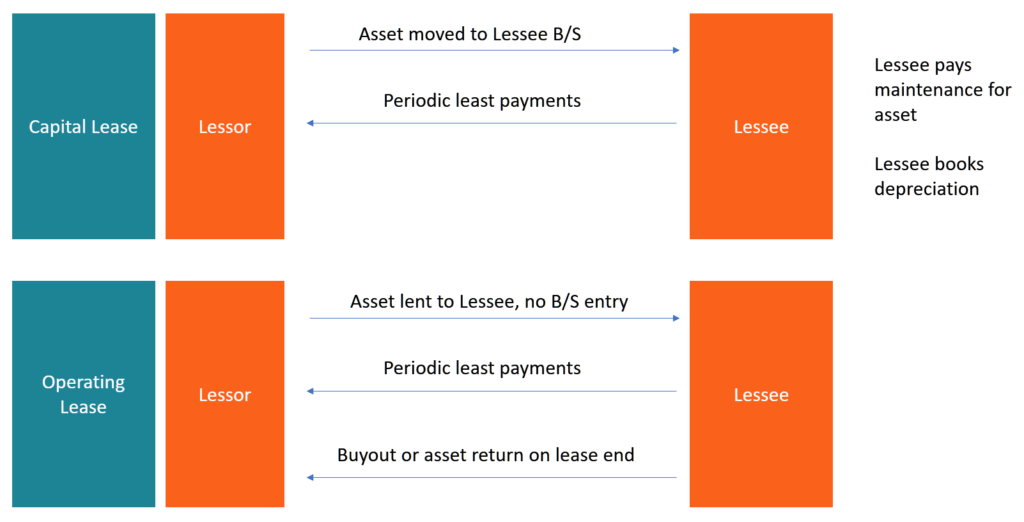

There are 2 types of leases defined in IFRS 16: A finance lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an underlying asset. An operating lease is a lease other than a finance lease.The lessor reports the lease as a leased asset on the balance sheet and individual lease payments as income on the income and cash flow statements. The lessee reports the lease as both an asset and a liability on the balance sheet due to their stake as a potential owner of the asset and their required payment.Operating leases are a form of “off balance sheet accounting” mechanism that allows a company to have a debt obligation that does NOT get disclosed on the company balance sheet. … Lease payments (i.e., rent) are liabilities, which can be considered debt. But the lease itself can actually be an asset.

:max_bytes(150000):strip_icc()/operating-lease-4191822-1-c4b12434faf241c1ba94b5709525034a.jpg)

How is a lease classified under IFRS 16 : Leases that transfer substantially all the risks and rewards of ownership of an asset were classified as finance leases. All other leases were classified as operating leases.

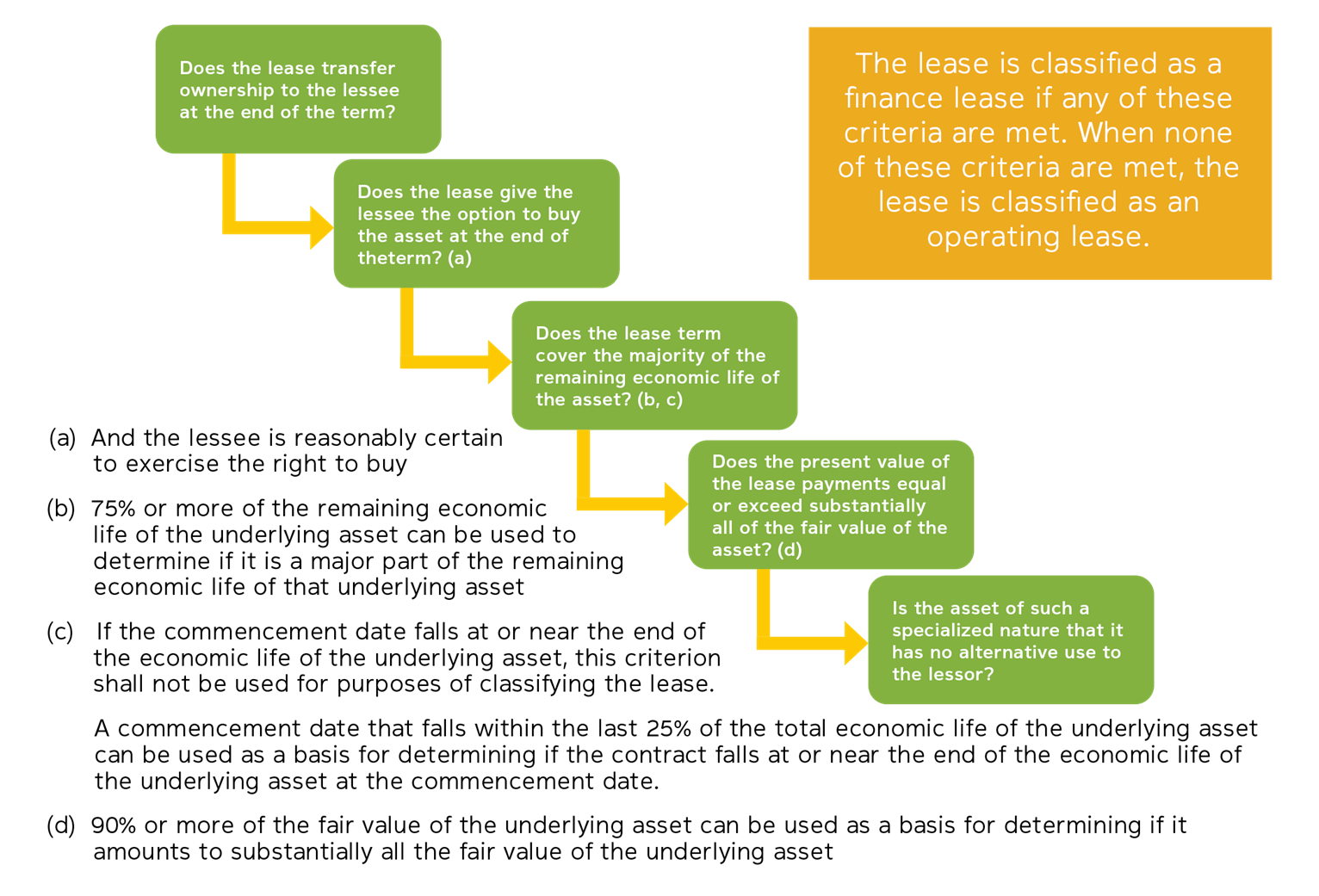

What are the 5 criteria for finance lease

If any one of these five criteria are met, at its inception, the lease should be considered a finance lease:

- Transfer of ownership. The lease transfers ownership of the property to Cornell by the end of the lease term.

- Lease purchase option.

- Lease term.

- Present value.

- Alternative use.

Is a finance lease an asset or liability : at commencement of the lease term, finance leases should be recorded as an asset and a liability at the lower of the fair value of the asset and the present value of the minimum lease payments (discounted at the interest rate implicit in the lease, if practicable, or else at the entity's incremental borrowing rate) [ …

They are recorded on the company's balance sheet; as a result, they can affect a company's financial ratios, such as debt-to-equity, return-on-assets, or solvency if companies use a significant amount of leased assets.

Likewise, operating leases do not need to be reported as a liability on the balance sheet, as they are not treated as debt. The firm does not record any depreciation for assets acquired under operating leases. However, if a lease does meet any of the above criteria, it is instead considered a capital lease.

How are leases classified

Under FASB ASC 840, a lessee can classify a lease as either an Operating lease or a Capital lease. Rent expense under an operating lease is generally recognized on a straight-line basis over the lease term regardless of the timing of the actual rental payments.IFRS 16 requires companies to recognize all leases on their balance sheets, regardless of whether they are operating or finance leases. This change has a significant impact on companies' financial statements, and it can also have an impact on their cash flow and profitability.To be classified as a finance lease, at least one of the following criteria must be true:

- A transferral of ownership of an asset to the lessee at the end of the term of the initial lease.

- The lessee is reasonably certain that they will exercise a purchase option at the end of the term of the lease.

Operating leases are assets rented by a business where ownership of the asset is not transferred when the rental period is complete.

What are the two major classifications of leases : The two most common types of leases are operating leases and financing leases (also called capital leases). In order to differentiate between the two, one must consider how fully the risks and rewards associated with ownership of the asset have been transferred to the lessee from the lessor.

How are finance leases accounted for : A company with a finance lease records an asset and its related liability on the balance sheet. It can deduct the computed interest component of the lease payments yearly on its income statement. It has full control of the asset it leased and is entirely responsible for its upkeep.

How to determine if a lease is capital or operating

Leases have two classifications under US GAAP . A capital lease, now known as a finance lease, resembles a financed purchase; the lease term spans most of the asset's useful life. An operating lease resembles a rental agreement in that the asset is used for a set time with useful life remaining at lease end.

With IFRS 16, lease liabilities for all (operational) leases are now recognized, which increases the numerator of the ratio. The total debt of the company will also increase because the recognized lease liabilities are included in the company's debt calculations.Operating leases and Finance leases are the two most common types of leases (also called capital leases). In order to distinguish between the two, it is important to understand how the costs and benefits associated with the possession of the asset have been fully transferred from the lessor to the lessee.

Who will classify leases as operating or finance lease in accounting under IFRS 16 : Lessors continue to classify leases as operating or finance, with IFRS 16's approach to lessor accounting substantially unchanged from its predecessor, IAS 17.