Antwort How do you determine if a lease is finance or operating? Weitere Antworten – How to determine if a lease is finance or operating

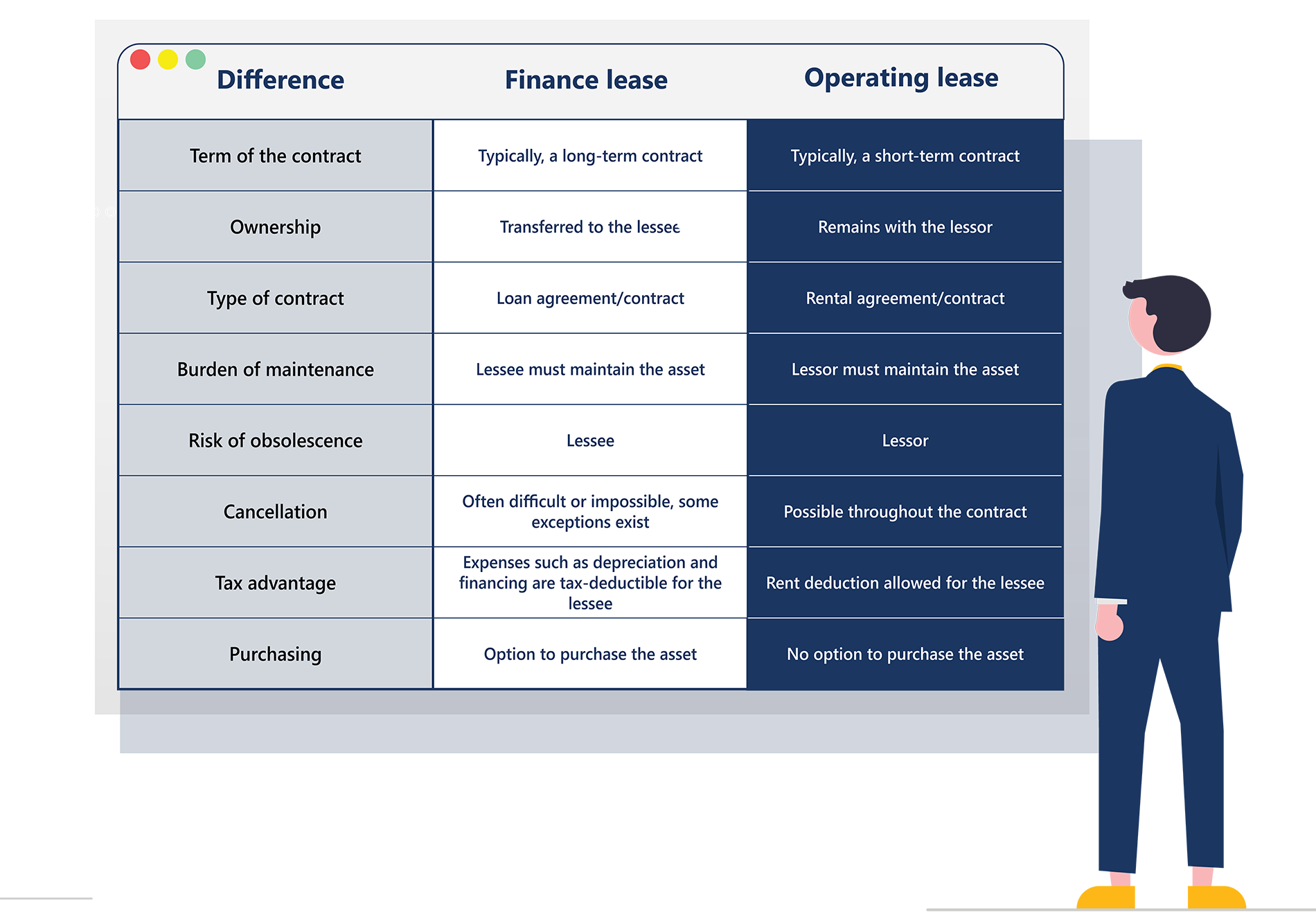

An operating lease is a contract that permits the use of an asset without transferring the ownership rights of said asset. A finance lease is a contract that permits the use of an asset and transfers ownership after the lease period is complete, and the lessor meets all other contract obligations.If the lease meets any of the criteria, then it must be recorded as a finance lease. The five criteria relates to a bargain purchase option, transfer of ownership, net present value of lease payments, economic life, and whether the asset is specialized.A lease is classified as a finance lease by a lessee and as a sales-type lease by a lessor if ownership of the underlying asset transfers to the lessee by the end of the lease term. This criterion is also met if the lessee is required to pay a nominal fee for the legal transfer of ownership.

When a lease qualifies as a finance lease : Transfer of title/ownership to the lessee

This criterion is the same from ASC 840 to ASC 842. If title transfers to the lessee, then the lease is classified as finance.

Does IFRS 16 distinguish between operating and finance leases

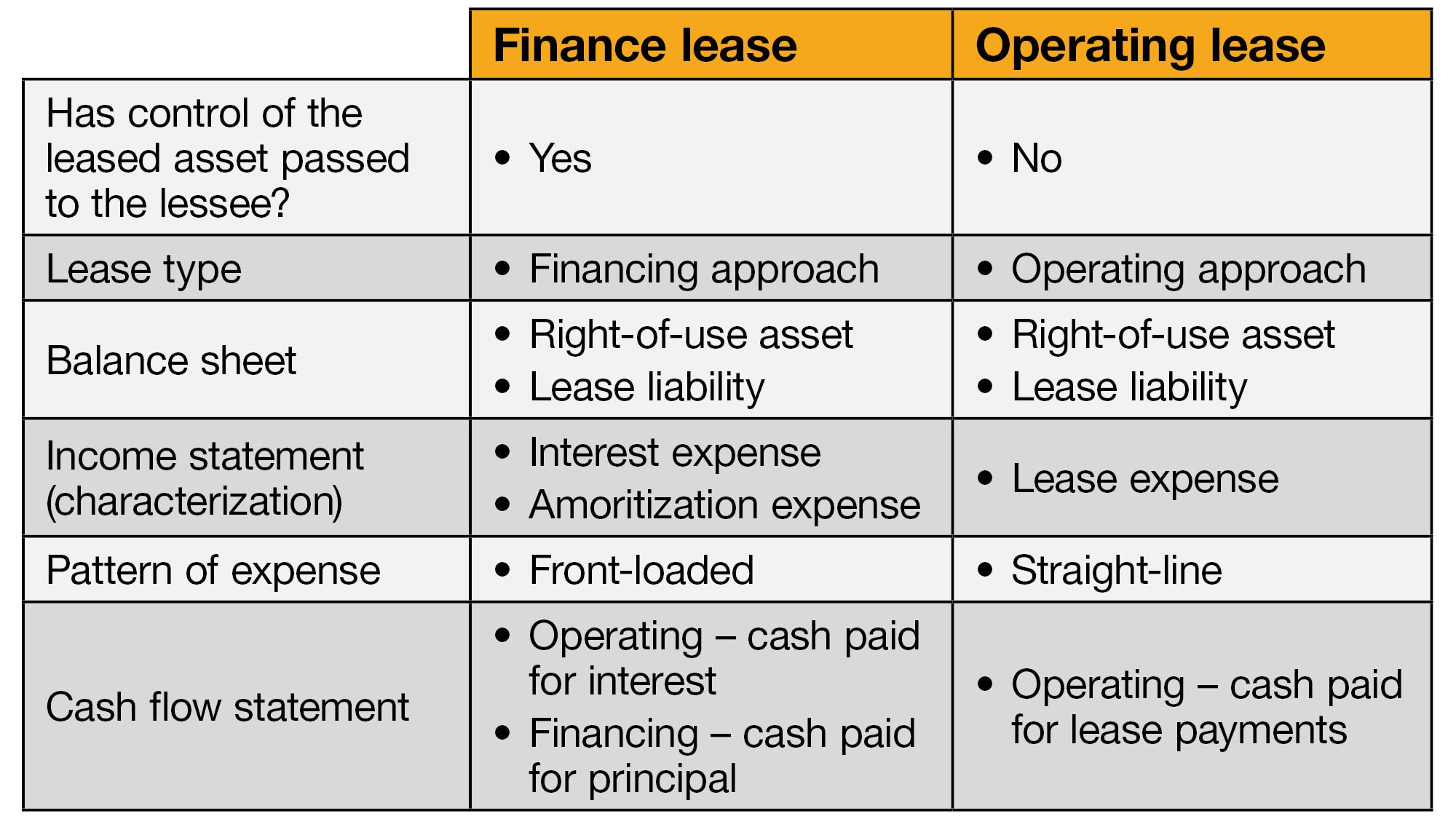

IFRS 16 eliminates the classification of leases as either operating leases or finance leases for a lessee. 3 Instead all leases are treated in a similar way to finance leases applying IAS 17.

What is an example of a finance lease : In the case of finance leases, where the relationship is more like ownership — meaning, the risks and control of the asset lies mostly with the lessee. An open-ended vehicle lease, where there is an obligation to purchase the car at the end of the lease, is an example of a finance lease.

For a lessor, a lease is financed if any of the following five criteria (IFRS 16.63) are met: (a) the lease transfers ownership of the underlying asset to the lessee by the end of the lease term; (b) the lessee has the option to purchase the underlying asset at a price that is expected to be sufficiently lower than the …

At the commencement of a finance lease, the lessor recognises a lease receivable that equates to the net investment in the lease (IFRS 16.67). The net investment in the lease comprises of the following components, discounted at the interest rate implicit in the lease: Lease payments receivable by a lessor, and.

What is the difference between finance and operating leases in IFRS 16

Classification of leases

There are 2 types of leases defined in IFRS 16: A finance lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an underlying asset. An operating lease is a lease other than a finance lease.A finance lease is one in which risks and rewards incidental to the ownership of the leased asset are transferred to the lessee but not the actual owner. Thus, in the case of a finance lease, we can say that notional ownership is passed to the lessee.If any one of these five criteria are met, at its inception, the lease should be considered a finance lease:

- Transfer of ownership. The lease transfers ownership of the property to Cornell by the end of the lease term.

- Lease purchase option.

- Lease term.

- Present value.

- Alternative use.

Paragraph 9 of IFRS 16 states that 'a contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration'.

What are the characteristics of an operating lease : Characteristics of a Operating Leases include:

Substantial transfer of risks and rewards remain with the lessor e.g. Maintenance, major repairs. Cannot contain a bargain purchase option. Less than 75% of the asset's estimated economic life. Lessee considered to be renting; lease payment treated as a rental expense.

How do you know if lease is under IFRS 16 : Paragraph 9 of IFRS 16 states that 'a contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration'.

What is the 90% rule in leasing

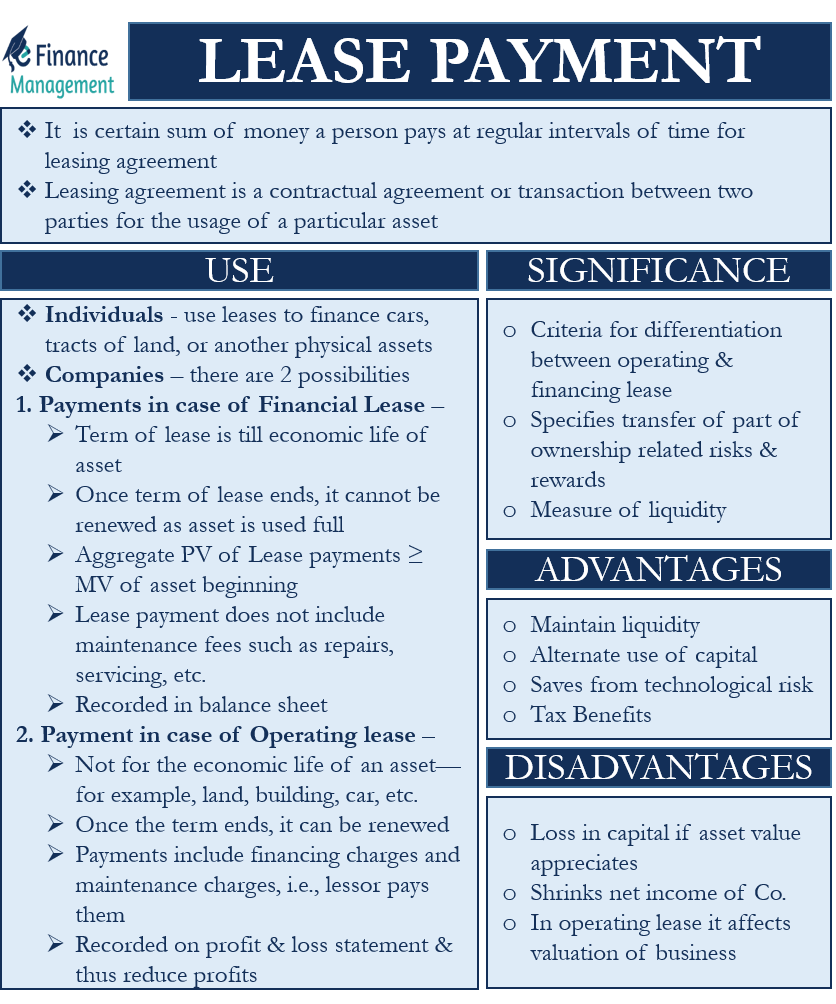

The lessee has the option to buy the asset at the end of the lease term at a bargain purchase price that is below the fair market value. The lessee gains ownership at the end of the lease period. The present value of lease payments must be greater than 90% of the asset's fair market value.

IFRS 16 eliminates the classification of leases as either operating leases or finance leases for a lessee. 3 Instead all leases are treated in a similar way to finance leases applying IAS 17.Accounting by lessors under IFRS 16

This means that IFRS 16 requires a lease: To be classified as a finance lease if substantially all of the risks and rewards incidental to ownership of the leased asset have been transferred to the lessee. To otherwise be classified as an operating lease.

What are the criteria for classifying a lease as operating : Operating Leases

Any lease that doesn't meet the criteria to be a finance lease is called an operating lease. If your lease is an operating lease, you must recognize a single lease expense, which is calculated to amortize the total cost of the lease over the lease term on a straight-line basis.