Antwort How do you get lease liability? Weitere Antworten – How to determine the lease liability

Lease liability measurement

According to ASC 842 and IFRS 16, the lease liability value is calculated with the following formula: The present value of the lease payments payable over the lease term. Discounted at the rate implicit in the lease.A lease liability is the financial obligation for the payments required by a lease, discounted to present value. Under ASC 842, IFRS 16, and GASB 87, the finance lease liability is calculated as the present value of the lease payments remaining over the lease term.Lease liability

The Lease Expense is the amount of straight-line rent expense over the term of the lease. The amount recorded on the Lease Liabilities account represents adjustments to arrive at the new net present value of the remaining payments.

How to calculate interest on lease liabilities : When calculating interest expense for a finance lease, the outstanding obligation is equal to the previous period's ending lease liability balance. Then the appropriate annual interest rate is multiplied by the fraction of one year for which the interest expense is being calculated.

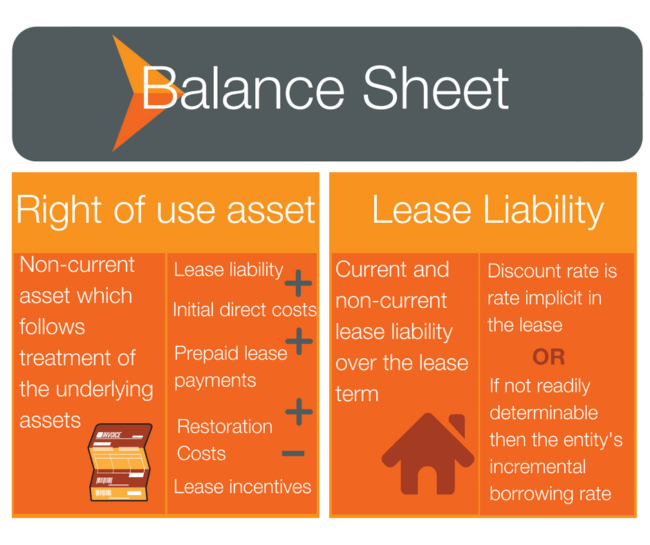

How do you calculate lease liability under IFRS 16

IFRS 16 requires that the lease liability should initially be measured at the present value of the lease payments that are not paid at the commencement date. The discount rate used to determine present value should be the rate of interest implicit in the lease.

How is Rou and lease liability calculated : How the ROU Asset Is Calculated. Generally, the ROU asset is calculated as the initial lease liability amount, plus any lease payments made to the lessor before the lease commencement date, any initial direct costs incurred, less any lease incentives received.

They are recorded on the balance sheet as a ROU asset and lease liability. Operating lease expense is still straight-lined over the lease term: Operating lease liability is accounted for the same way as a finance lease, using an amortized cost basis.

Since the lease is classified as a finance lease, the company must first calculate the net present value of future minimum lease payments. Once the company has that figure, the debit would be to Right of Use asset, with the credit to lease liability.

Is lease liability a fixed asset

Balance Sheet: The leased asset is recorded as a fixed asset, and a corresponding lease liability is recognized on the balance sheet. Income Statement: The lessee will report interest expense on the lease liability and depreciation expense on the leased asset.

- Step 1 – Work Out Future Lease Payments.

- Step 2 – Determine the Discount Rate and Calculate the Lease Liability.

- Step 3 – Calculate the Right-of-Use Asset Value.

- Step 4 – Calculate the Unwinding of the Lease Liability.

- Step 5 – Calculate the Right-of-Use Asset Amortization Rate.

Determine the Initial Right-of-Use Asset: The initial right-of-use asset is typically equal to the lease liability, adjusted for any lease payments made before or at the lease commencement date, initial direct costs, and any lease incentives received.

Audit procedures include:

- Agree on lease classification (operating vs finance lease)

- Recalculate right-of-use assets and lease liabilities.

- Test key estimates/judgments like discount rates and lease terms.

- Review amortization/interest calculations for accuracy.

- Assess impairment testing methodology and assumptions.

Is lease liability the same as debt : The liability associated with an Operating Lease (FASB only) IS NOT CONSIDERED DEBT, while the liability of a Finance Lease IS CONSIDERED DEBT.

How is lease liability classified in balance sheet : The liability for a leased asset should be presented separately in the balance sheet as a current liability or a long-term liability as the case may be.

What is the IFRS 16 lease liability

IFRS 16 introduces a single lessee accounting model and requires a lessee to recognise assets and liabilities for all leases with a term of more than 12 months, unless the underlying asset is of low value.

In broad terms, you calculate a lease by determining and adding the depreciation fee, plus a monthly sales tax and a financing fee. If you're looking to calculate your payment manually, here is the formula: Start with the sticker price (MSRP) of the car. Take the MSRP and multiply it by the residual percentage.The lease liability is the present value of the future lease payments and is recorded alongside the right-of-use asset for operating and finance leases. Under ASC 842, the lease liability is not considered debt. Under IFRS 16 and GASB 87, however, a lease liability is considered long-term debt.

Are lease liabilities a borrowing : Ind AS 116 requires lease liabilities to be disclosed separately from other liabilities either in the balance sheet or in the notes to accounts. It does not require such financial liabilities to be termed as borrowings; Schedule III requires finance lease obligation to be disclosed under borrowings.