Antwort What are all leases classified as? Weitere Antworten – How is a lease classified under IFRS 16

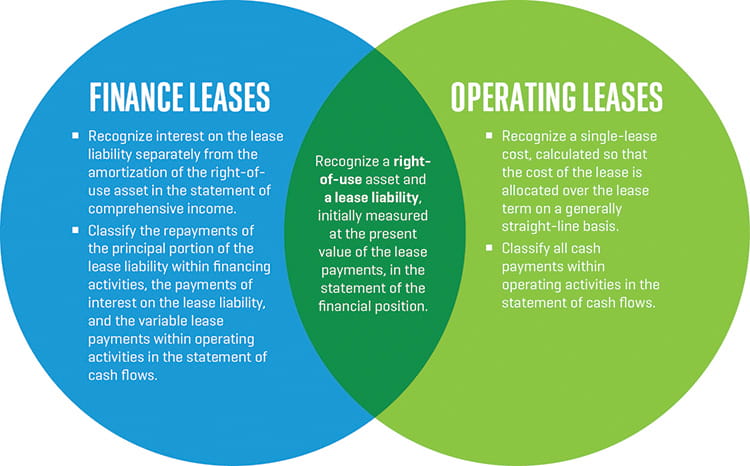

There are 2 types of leases defined in IFRS 16: A finance lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an underlying asset. An operating lease is a lease other than a finance lease.IFRS 16

Overview. IFRS 16 specifies how an IFRS reporter will recognise, measure, present and disclose leases. The standard provides a single lessee accounting model, requiring lessees to recognise assets and liabilities for all leases unless the lease term is 12 months or less or the underlying asset has a low value.Exploring what are the 3 main types of lease agreements

| Type | Duration | Recorded in Balance Sheet |

|---|---|---|

| Operating Lease | Short-to-Medium | No |

| Finance Lease | Long Term | Yes (Lessee) |

| Sale and Leaseback | Depending on Agreement | Contingent |

What are leases in accounting : Leases are contracts in which the property/asset owner allows another party to use the property/asset in exchange for some consideration, usually money or other assets. The two most common types of leases in accounting are operating and finance (or capital) leases.

Does IFRS 16 apply to all leases

IFRS 16 introduces a single lessee accounting model and requires a lessee to recognise assets and liabilities for all leases with a term of more than 12 months, unless the underlying asset is of low value.

Are all leases capitalized under IFRS 16 : On 13 January 2016, the International Accounting Standards Board (IASB) issued IFRS 16 Leases, which essentially does away with operating leases and, subject to limited exceptions, requires all leases to be capitalised on the balance sheet.

All leases (with limited exception) are recorded “on balance sheet”, similar to finance/capital lease treatment under ASPE. The assets arising from leases under IFRS 16 are known as “right-of-use” assets. determine. to renew or extend the lease at the end of the lease term.

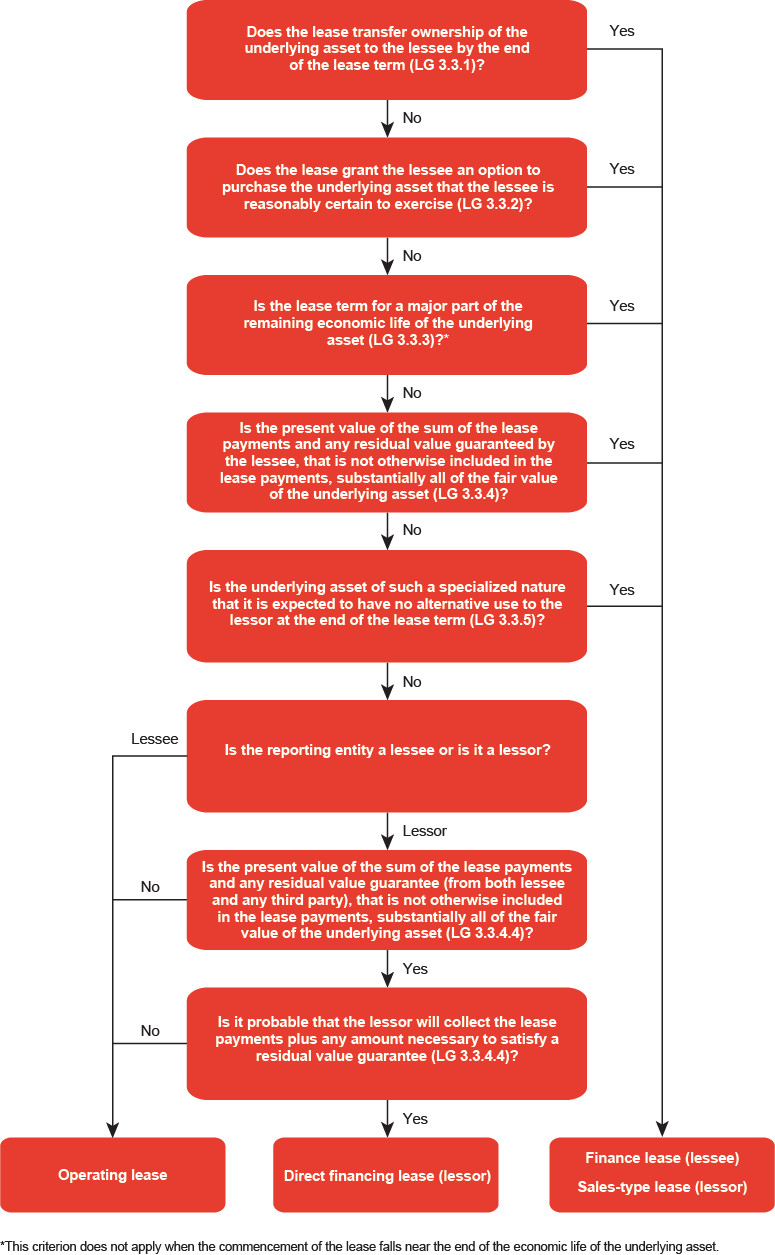

A lease is classified as a finance lease by a lessee and as a sales-type lease by a lessor if ownership of the underlying asset transfers to the lessee by the end of the lease term.

What are the two major classifications of leases

Leases have two classifications under US GAAP . A capital lease, now known as a finance lease, resembles a financed purchase; the lease term spans most of the asset's useful life. An operating lease resembles a rental agreement in that the asset is used for a set time with useful life remaining at lease end.Accounting for a finance lease has four steps:

- Record the present value of all lease payments as the cost of the lease.

- Record only the interest portion of each payment as an expense.

- Depreciate the recognised cost of the asset over its applicable life.

- Recognise the asset's disposal upon its retirement.

If you use what's called a capital or finance lease, you report the leased property on your balance sheet as if it were an asset you own. If you have an operating lease, you record it as a liability.

:max_bytes(150000):strip_icc()/operating-lease-4191822-1-c4b12434faf241c1ba94b5709525034a.jpg)

IFRS 16 offers two optional exemptions from recognition of right-of-use assets and lease liabilities. The first is an exemption from short-term leases, and the second is the exemption from leases of low value assets.

What is the difference between IAS 17 and IFRS 16 finance lease : This is because, applying IFRS 16, a company presents the implicit interest in lease payments for former off balance sheet leases as part of finance costs. In contrast, under IAS 17, the entire expense related to off balance sheet leases is included as part of operating expenses.

Should leases be capitalized or expensed : A lessee must capitalize leased assets if the lease contract entered into satisfies at least one of the four criteria published by the Financial Accounting Standards Board (FASB). An operating lease expenses the lease payments immediately, but a capitalized lease delays recognition of the expense.

What are the 5 lease classification tests

If the lease meets any of the criteria, then it must be recorded as a finance lease. The five criteria relates to a bargain purchase option, transfer of ownership, net present value of lease payments, economic life, and whether the asset is specialized.

The three most common types of leases are gross leases, net leases, and modified gross leases.

- The Gross Lease. The gross lease tends to favor the tenant.

- The Net Lease. The net lease, however, tends to favor the landlord.

- The Modified Gross Lease.

In some cases, fluctuations in the fair value of the residual interest in the leased asset are passed back to the lessee. This indicates that the lessee is bearing the residual value risk, and the lessor's return on investment is effectively fixed. These indicators provide evidence of a finance lease.

Is an operating lease an asset : Operating leases are assets rented by a business where ownership of the asset is not transferred when the rental period is complete.