Antwort What are the two types of lease classifications for a lessee? Weitere Antworten – What are the classification of leases in IFRS 16

Classification of leases

There are 2 types of leases defined in IFRS 16: A finance lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an underlying asset. An operating lease is a lease other than a finance lease.IFRS 16 introduces a single lessee accounting model and requires a lessee to recognise assets and liabilities for all leases with a term of more than 12 months, unless the underlying asset is of low value.Under IFRS 16, lessors account for finance leases by initially derecognising the asset and recognising a receivable for the net investment in the lease. Initial direct costs (other than those incurred by a manufacturer or dealer lessor) are included in the net investment in the lease.

What is the difference between IAS 17 and IFRS 16 : Under IAS 17, leases are classified as either Finance Lease or Operating Lease based on the risks and rewards incidental to ownership of the asset. Under IFRS 16, all leases are classified as Finance Leases, and the lessee is required to RECOGNIZE a lease liability and a Right of Use (RoU) asset.

What are the 2 categories for all leases

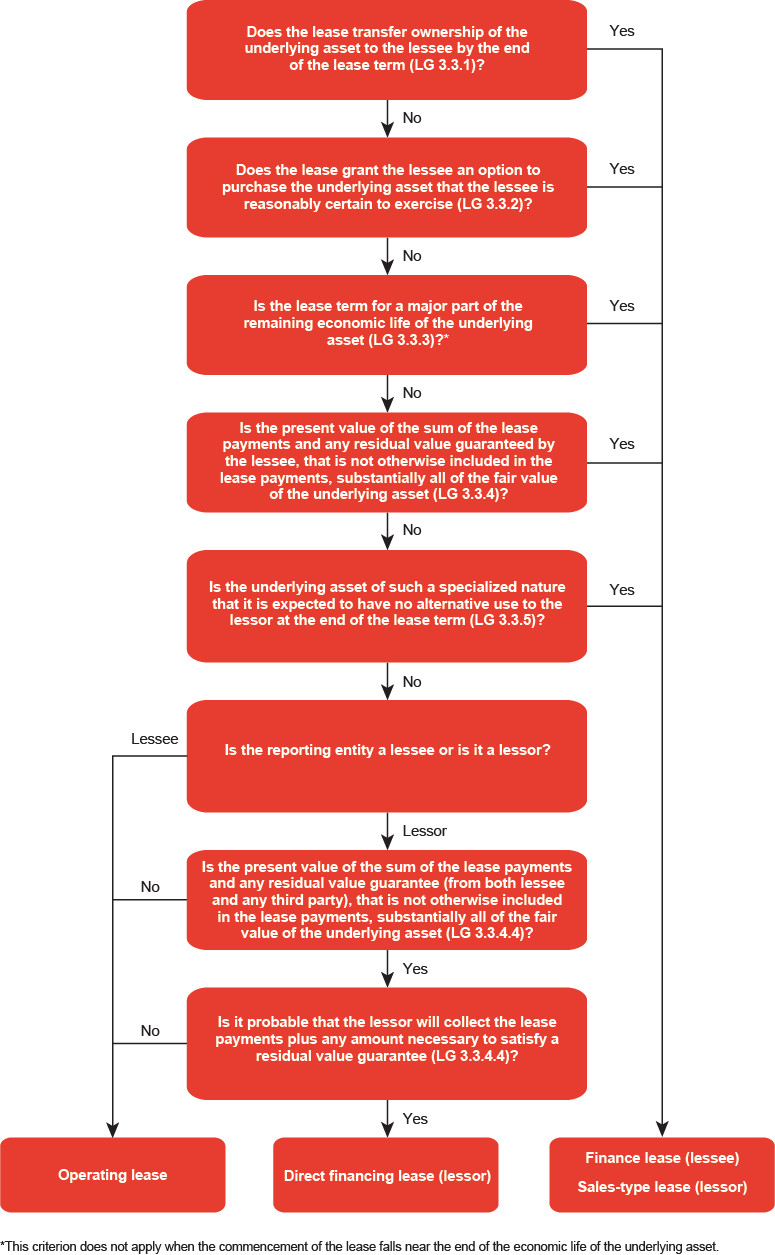

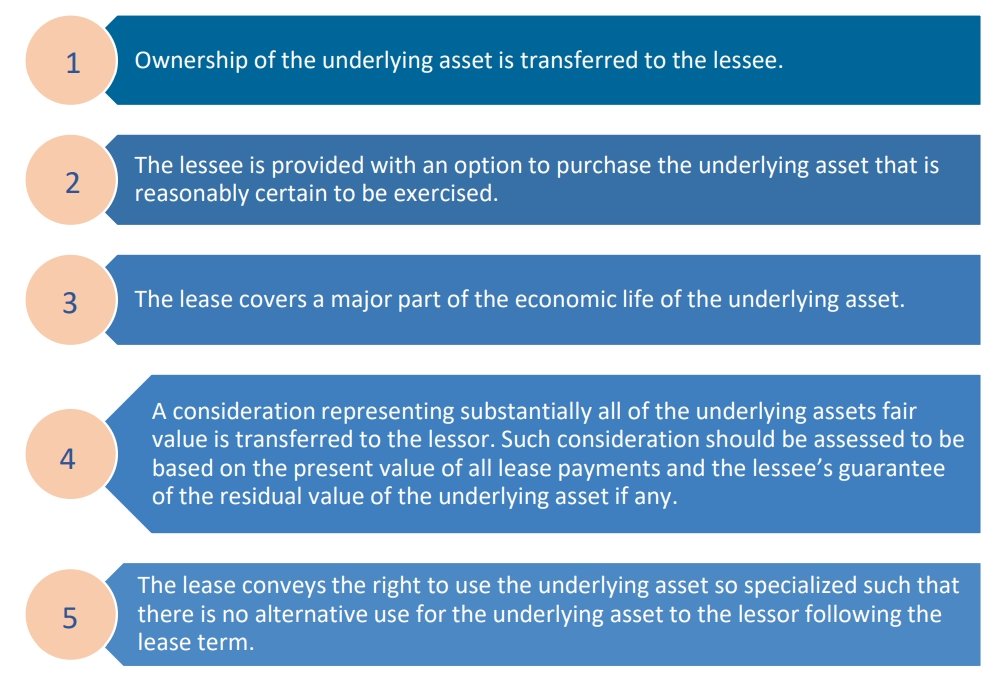

A lease is classified as a finance lease by a lessee and as a sales-type lease by a lessor if ownership of the underlying asset transfers to the lessee by the end of the lease term.

What are the two types of leases under IFRS : a finance lease if the lease transfers substantially all the risks and rewards incidental to ownership; and. an operating lease if the lease does not transfer substantially all the risks and rewards incidental to ownership.

Paragraph 9 of IFRS 16 states that 'a contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration'.

Lessee accounting under updated accounting standards

Lessees are required to recognize nearly all leases (with some exceptions, like short-term leases) on the balance sheet. This represents a significant shift from previous guidelines, where only capital leases were recognized.

What is the classification of lease for lessor

In accordance with IFRS 16.61, a lessor should classify each of its leases as either a finance lease or an operating lease. Leases that transfer substantially all of the risks and rewards incidental to ownership of the underlying asset are finance leases, and all other leases are operating leases.Leases are required to be classified as either finance leases (which transfer substantially all the risks and rewards of ownership, and give rise to asset and liability recognition by the lessee and a receivable by the lessor) and operating leases (which result in expense recognition by the lessee, with the asset …One of the most significant changes to the IFRS in recent years is the introduction of IFRS 16, which deals with lease accounting. This new standard replaced IAS 17, which had been in use for several decades.

IFRS 16 provides an option to lessees with short-term leases to account for them as operating leases, as they were accounted for under IAS 17 that is off balance sheet. Same option is provided also for leases where the underlying asset is of low-value.

What is the lease classification for a lessee : Under FASB ASC 842, a lessee can classify a lease as either an Operating lease or a Finance lease.

What is the classification of a lease : A lease is classified as a finance lease by a lessee and as a sales-type lease by a lessor if ownership of the underlying asset transfers to the lessee by the end of the lease term. This criterion is also met if the lessee is required to pay a nominal fee for the legal transfer of ownership.

What are the two types of leases

The two most common types of leases are operating leases and financing leases (also called capital leases). In order to differentiate between the two, one must consider how fully the risks and rewards associated with ownership of the asset have been transferred to the lessee from the lessor.

Who does IFRS 16 apply to Initially, at least, these changes will only apply to organisations that already report using IFRS, typically international companies or PLCs. The majority of SMEs report to the UK's generally accepted accounting principles (UK GAAP) and this is unlikely to change until around 2022/23.Under ASC 842, lessees are required to classify leases into, Finance Lease, and Operating lease, while lessors are required to classify leases into, Sales-Type Lease, Direct Financing Lease, and Operating Lease.

What are the classifications of leases : Leases are required to be classified as either finance leases (which transfer substantially all the risks and rewards of ownership, and give rise to asset and liability recognition by the lessee and a receivable by the lessor) and operating leases (which result in expense recognition by the lessee, with the asset …