Antwort What is the liability of a lease? Weitere Antworten – What are the liabilities of a lease

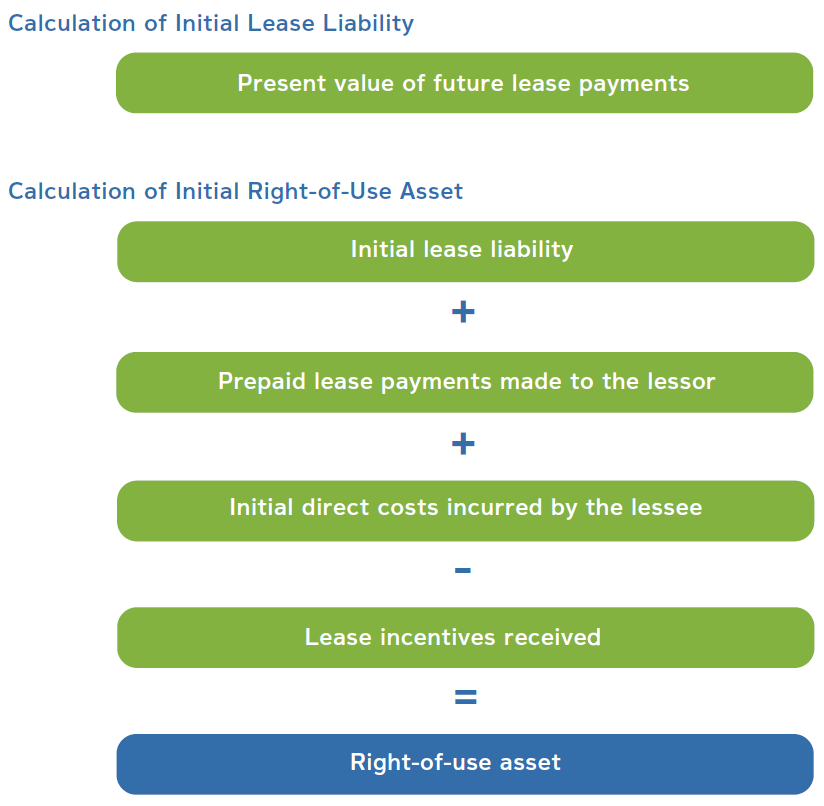

A lease liability is the financial obligation for the payments required by a lease, discounted to present value. Under ASC 842, IFRS 16, and GASB 87, the finance lease liability is calculated as the present value of the lease payments remaining over the lease term.Lease liability measurement

According to ASC 842 and IFRS 16, the lease liability value is calculated with the following formula: The present value of the lease payments payable over the lease term. Discounted at the rate implicit in the lease.These liabilities represent the present value of future lease payments to be made over the lease term. This increases the total liabilities reported on the balance sheet. The amount of the liability is determined by discounting future lease payments using the interest rate implicit in the lease.

Is a lease recorded as a liability : at commencement of the lease term, finance leases should be recorded as an asset and a liability at the lower of the fair value of the asset and the present value of the minimum lease payments (discounted at the interest rate implicit in the lease, if practicable, or else at the entity's incremental borrowing rate) [ …

Is lease liability a fixed asset

Balance Sheet: The leased asset is recorded as a fixed asset, and a corresponding lease liability is recognized on the balance sheet. Income Statement: The lessee will report interest expense on the lease liability and depreciation expense on the leased asset.

Is lease liability financial or non financial : As the ROU asset is a non-financial asset, it is accounted for consistently with other non-financial assets. As the lease liability is a financial liability, it is accounted for consistently with other financial liabilities.

The liability associated with an Operating Lease (FASB only) IS NOT CONSIDERED DEBT, while the liability of a Finance Lease IS CONSIDERED DEBT.

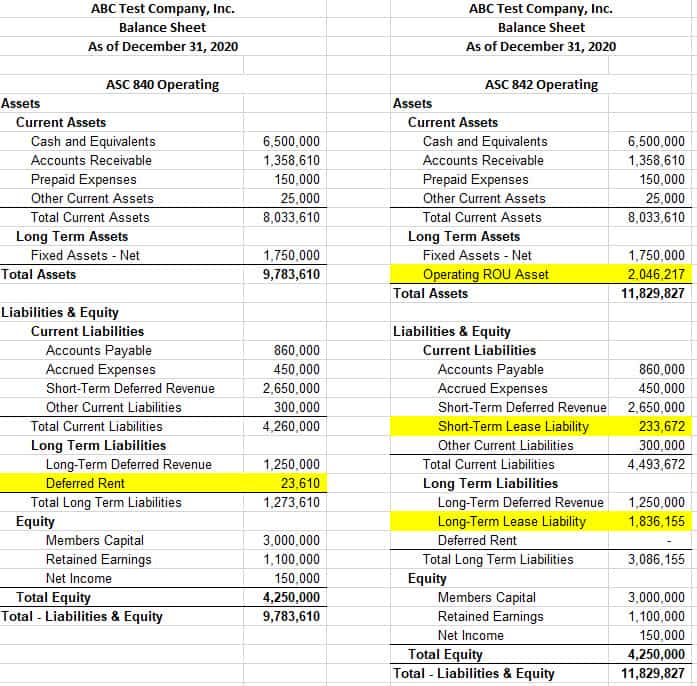

Operating leases are shown as an asset on the balance sheet, valued as the present value of the lease payments (not the market value of the asset). The lease liability is shown on the balance sheet (similarly, the present value of the lease payments).

Is lease liability a monetary liability

The liability to make lease payments is a monetary liability, and the right-of-use asset is a non- monetary asset.On the lease commencement date, a lessee is required to measure and record a lease liability equal to the present value of the remaining lease payments, discounted using the rate implicit in the lease (or if that rate cannot be readily determined, the lessee's incremental borrowing rate).Operating leases are shown as an asset on the balance sheet, valued as the present value of the lease payments (not the market value of the asset). The lease liability is shown on the balance sheet (similarly, the present value of the lease payments).

The lease liability is the present value of the future lease payments and is recorded alongside the right-of-use asset for operating and finance leases. Under ASC 842, the lease liability is not considered debt. Under IFRS 16 and GASB 87, however, a lease liability is considered long-term debt.

Is lease liability intangible : Because tangible property cannot be a liability, this further suggests that leases are intangible property.

Is lease liability a debit or credit : Since the lease is classified as a finance lease, the company must first calculate the net present value of future minimum lease payments. Once the company has that figure, the debit would be to Right of Use asset, with the credit to lease liability.

Are lease liabilities funded debt

On the balance sheet, the finance leased asset is typically recorded as part of property, plant and equipment (PP&E), and the lease liability is recorded as funded debt.

Lease liabilities and receivables under a finance lease also classify as financial instruments (IAS 32. AG9). The following are examples of items that are not financial instruments: intangible assets, inventories, right-of-use assets, prepaid expenses, deferred revenue, warranty obligations (IAS 32.Since a lessee's lease liability is a monetary item, the liability is translated using a current exchange rate at the end of each reporting period and foreign exchange differences are recognised in profit or loss.

Are lease liabilities debt : The liability associated with an Operating Lease (FASB only) IS NOT CONSIDERED DEBT, while the liability of a Finance Lease IS CONSIDERED DEBT.