Antwort What leases fall under IFRS 16? Weitere Antworten – What qualifies as a lease under IFRS 16

The definition of a lease

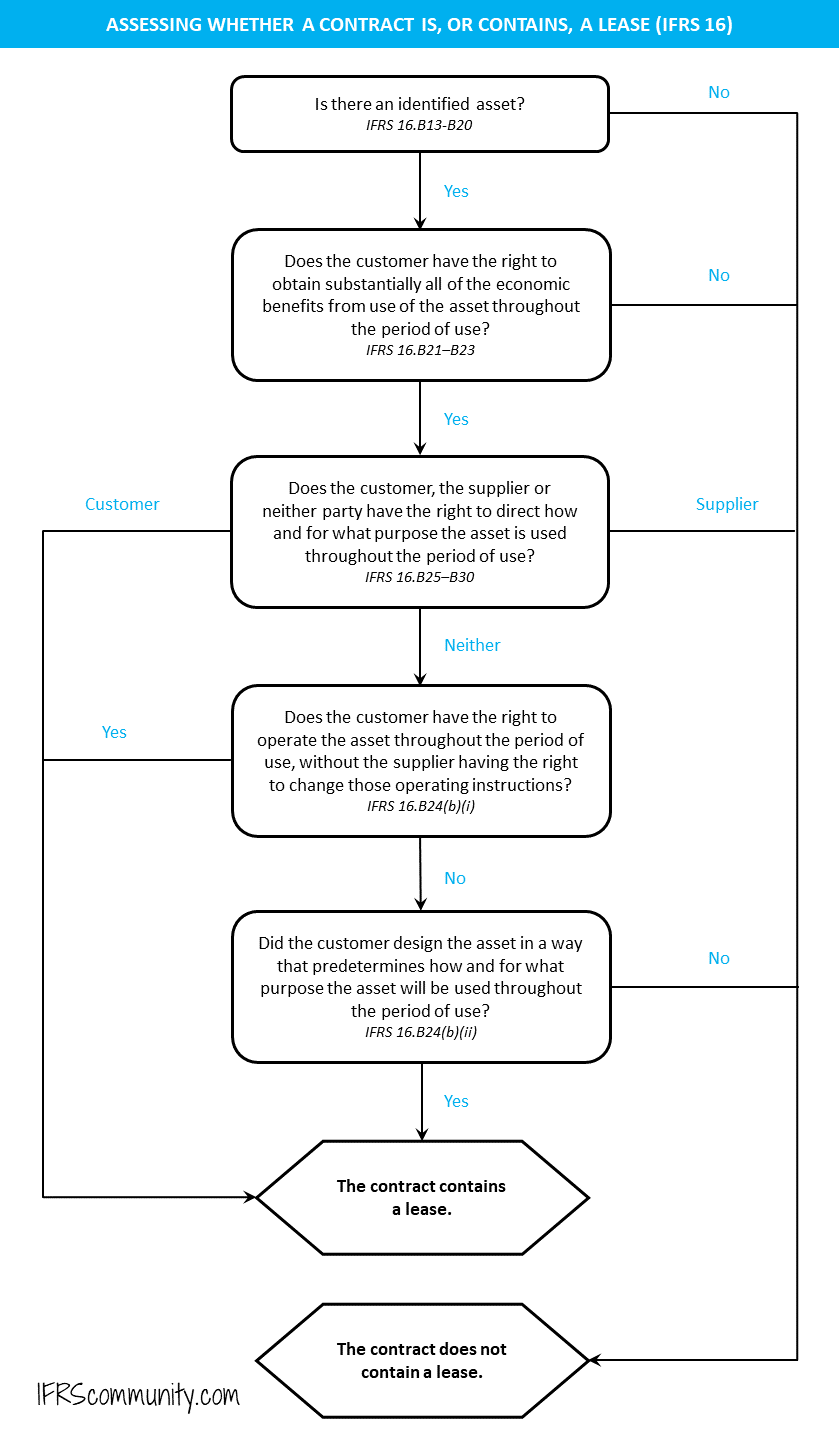

Paragraph 9 of IFRS 16 states that 'a contract is, or contains, a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration'.Who does IFRS 16 apply to Initially, at least, these changes will only apply to organisations that already report using IFRS, typically international companies or PLCs. The majority of SMEs report to the UK's generally accepted accounting principles (UK GAAP) and this is unlikely to change until around 2022/23.IFRS 16 offers two optional exemptions from recognition of right-of-use assets and lease liabilities. The first is an exemption from short-term leases, and the second is the exemption from leases of low value assets. Key learning objectives: Identify the two IFRS 16 exemptions, and explain why they are exempt.

How are leases treated under IFRS 16 : Under IFRS 16 lessees may elect not to recognise assets and liabilities for leases with a lease term of 12 months or less. In such cases a lessee recognises the lease payments in profit or loss on a straight-line basis over the lease term. The exemption is required to be applied by class of underlying assets.

What is the IFRS 16 criteria for leases

IFRS 16 introduces a single lessee accounting model and requires a lessee to recognise assets and liabilities for all leases with a term of more than 12 months, unless the underlying asset is of low value.

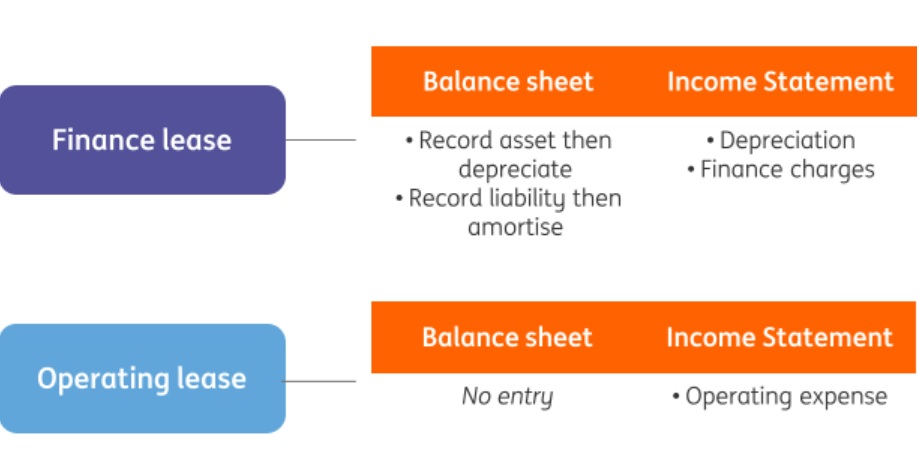

How is a lease classified under IFRS 16 : There are 2 types of leases defined in IFRS 16: A finance lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an underlying asset. An operating lease is a lease other than a finance lease.

IFRS 16 introduces a single lessee accounting model and requires a lessee to recognise assets and liabilities for all leases with a term of more than 12 months, unless the underlying asset is of low value.

Leases of intangible assets

Rights for intangible assets such as films, recordings, plays, patents, and copyrights are not covered by IFRS 16, as indicated in IFRS 16.3(e).

How are leases recognized under IFRS 16

Overview. IFRS 16 specifies how an IFRS reporter will recognise, measure, present and disclose leases. The standard provides a single lessee accounting model, requiring lessees to recognise assets and liabilities for all leases unless the lease term is 12 months or less or the underlying asset has a low value.Under IFRS 16 a lease is defined as 'a contract, or part of a contract, that conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration'. A contract can be (or contain) a lease only if the underlying asset is 'identified'.There are 2 types of leases defined in IFRS 16: A finance lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an underlying asset. An operating lease is a lease other than a finance lease.

Rights for intangible assets such as films, recordings, plays, patents, and copyrights are not covered by IFRS 16, as indicated in IFRS 16.3(e).

What is included in lease payments IFRS 16 : Lease payments used to measure the lease liability at commencement date include the following (to the extent they have not yet been paid): fixed payments – including in-substance fixed payments less any lease incentives receivable. variable lease payments that depend on an index or a rate.

Do operating leases exist under IFRS 16 : IFRS 16 eliminates the classification of leases as either operating leases or finance leases for a lessee. 3 Instead all leases are treated in a similar way to finance leases applying IAS 17.

How to determine if a lease is finance or operating

An operating lease is a contract that permits the use of an asset without transferring the ownership rights of said asset. A finance lease is a contract that permits the use of an asset and transfers ownership after the lease period is complete, and the lessor meets all other contract obligations.

IFRS 16 introduces a single lessee accounting model and requires a lessee to recognise assets and liabilities for all leases with a term of more than 12 months, unless the underlying asset is of low value.Leases of intangible assets

Rights for intangible assets such as films, recordings, plays, patents, and copyrights are not covered by IFRS 16, as indicated in IFRS 16.3(e). Such rights are governed by IAS 38. However, for other intangible assets, lessees can opt to apply either IAS 38 or IFRS 16 (IFRS 16.4).

Does IFRS 16 distinguish between operating and finance leases : IFRS 16 eliminates the classification of leases as either operating leases or finance leases for a lessee. 3 Instead all leases are treated in a similar way to finance leases applying IAS 17.